Found your dream home but haven’t sold yours? A Bridge Loan for Real Estate solves the timing gap. We break down the costs, risks, and when to use this powerful tool.

Table of Contents

I’ll never forget a couple I worked with a few years back, let’s call them Sarah and Mark. They had outgrown their starter home and spent six months hunting for the perfect upgrade. Finally, they found it—a sprawling colonial with the exact kitchen island Sarah wanted. They put in an offer immediately.

There was just one problem: their current house wasn’t even listed yet.

They included a “sale contingency” in their offer, meaning they would only buy the new house if they sold their old one first. The seller rejected them instantly. Why? Because in a hot market, sellers don’t wait. A cash buyer swooped in, and Sarah and Mark lost the house. They were devastated.

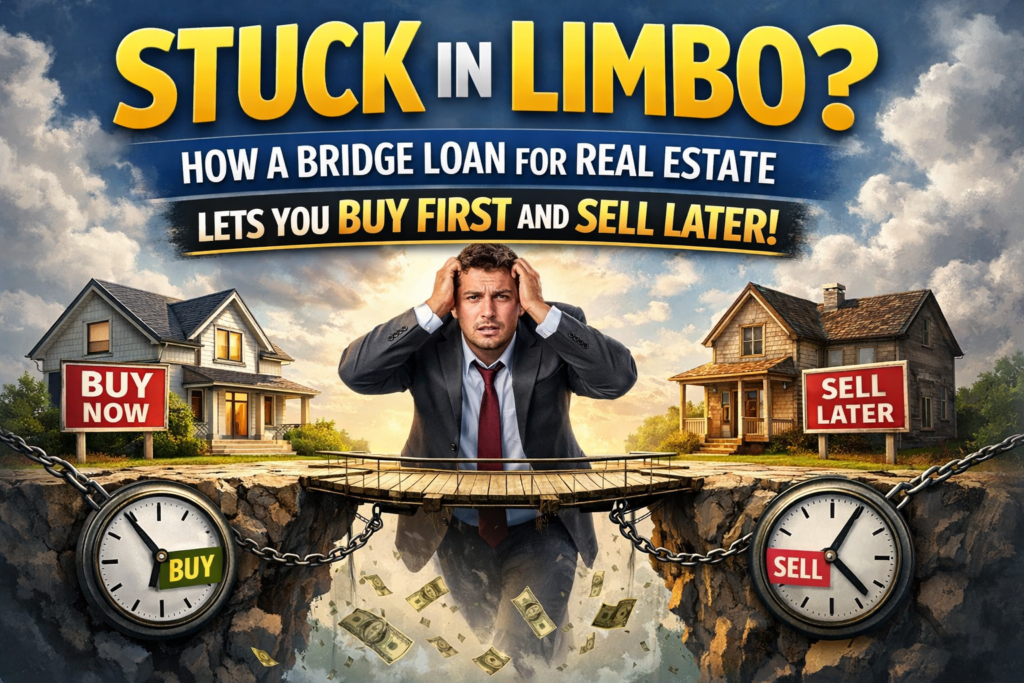

This is the classic real estate Catch-22. You need the equity from your old home to buy the new one, but you can’t get that money until you sell. It feels like you need to be in two places at once.

This is exactly where a Bridge Loan for Real Estate comes into play. It’s a tool designed specifically to break that deadlock. It isn’t for everyone—it’s expensive and risky—but when used correctly, it is the ultimate stress-reliever. If you are terrified of becoming homeless between transactions, let’s talk about how this gap financing strategy works.

What Exactly is a Bridge Loan?

Think of a Bridge Loan for Real Estate as a temporary lifeline. It bridges the gap (pun intended) between buying your new home and selling your old one.

Technically speaking, it is a short-term loan, usually lasting six to 12 months, that allows you to tap into the equity of your current home to fund the down payment and closing costs on your new home. Instead of waiting for your sale to close to get your cash, the lender fronts you the money.

This turns you into a non-contingent buyer. When you walk into a negotiation with a Bridge Loan for Real Estate in your back pocket, you are effectively a cash buyer in the eyes of the seller. You can close on their timeline, not yours. In a bidding war, that power is often worth more than a higher offer price.

How Does the Math Work?

Let’s look at the mechanics, because this is where people get confused. You typically take out a Bridge Loan for Real Estate against your current property (the one you are selling).

Let’s say your current home is worth $500,000, and you owe $200,000 on the mortgage. You have $300,000 in equity sitting there, trapped in drywall and landscaping. A lender might give you a bridge loan for 80% of your home’s value combined (Combined Loan-to-Value or CLTV). They give you the cash to put 20% down on the new house.

Now, you own two houses.

- The Old House: You still have your original mortgage payment + the bridge loan payment (often interest-only).

- The New House: You have your new mortgage payment.

Yes, it can be scary. You are technically carrying three financial obligations at once. However, most Bridge Loan for Real Estate structures are designed so you don’t make monthly payments on the bridge portion immediately; instead, it gets paid off in one lump sum when your old house finally sells.

The Cost of Convenience

I have to be honest with you—this convenience isn’t cheap. A Bridge Loan for Real Estate is a specialized product, and lenders charge a premium for the risk they are taking.

- Interest Rates: Expect to pay significantly higher rates than a standard 30-year fixed mortgage. We are talking usually 2% to 4% higher than the going rate.

- Origination Fees: Lenders often charge hefty administrative fees, sometimes up to 3% of the loan amount.

- Closing Costs: You are closing a loan, so you have appraisal fees and title fees again.

You are essentially paying a “convenience fee” to avoid moving into a rental apartment for three months or living in your in-laws’ basement. For many of my clients, paying $5,000 in fees is worth saving their sanity and securing their dream home.

Link to Bankrate: What is a bridge loan and how does it work?

When Should You Use a Bridge Loan for Real Estate?

This isn’t a tool you use just for fun. You use it when the market demands it. Here are the scenarios where I recommend it:

1. The Seller’s Market Squeeze

In a seller’s market, inventory is low. If you find a house you love, there are probably five other people who love it too. If you go in with a “home sale contingency,” your offer goes to the bottom of the pile. Using a Bridge Loan for Real Estate cleans up your offer and makes you competitive against cash buyers.

2. The Fixer-Upper Scenario

Maybe the new house needs work before you can move in. You can’t live there yet, but you need to sell your old house to pay for the renovation. A bridge loan lets you hold onto your old house (and live in it) while you renovate the new one. Once the new place is ready, you move, sell the old place, and pay off the loan.

3. Avoiding the “Double Move”

Moving is terrible. Moving twice is torture. Without gap financing, many people sell their home, move into a short-term rental/storage unit, wait to close on the new house, and move again. A Bridge Loan for Real Estate allows for a seamless transition: Old House -> New House. One moving truck. Done.

The Risks: What Could Go Wrong?

I’m risk-averse, so I always walk my clients through the worst-case scenario. The biggest risk with a Bridge Loan for Real Estate is that your old home doesn’t sell.

Most bridge loans have a term of 6 to 12 months. If the market tanks and your house sits on the market for a year, the bridge loan comes due. You might be forced to lower your asking price desperately just to pay off the loan. Also, qualifying can be tough. Lenders look at your “Debt-to-Income” (DTI) ratio. Since you are technically carrying two mortgages, your income needs to be high enough to support that debt load on paper, even if it’s just temporary.

Bridge Loan vs. HELOC: What’s the Difference?

Clients often ask, “Can’t I just use a Home Equity Line of Credit (HELOC)?” Yes, you can, but it’s tricky. A HELOC is cheaper. The interest rates are lower, and closing costs are minimal. However, many banks will freeze your HELOC if they know you are putting the house on the market. They don’t want to lend on an asset that is about to be sold. A Bridge Loan for Real Estate is explicitly designed for the sale. The lender wants you to sell.

If you have a lot of equity and open a HELOC before you decide to move, that can work. But once the “For Sale” sign is in the yard, the Bridge Loan for Real Estate is usually your only option for tapping equity.

Link to NerdWallet: Bridge Loans vs. HELOCs

How to Get Approved

Finding these loans can be harder than finding a standard mortgage. Big banks (like Chase or Wells Fargo) often don’t offer them because they are risky. You usually have to look at:

- Local Credit Unions: They have more flexibility with their portfolio.

- Hard Money Lenders: These are private investors. They move fast but charge high rates.

- Specialized Mortgage Brokers: They have access to niche lenders who love bridge products.

To get approved for a Bridge Loan for Real Estate, you need significant equity. If you only own 10% of your home, you won’t qualify. You typically need at least 20% to 30% equity to make the math work.

Is It Worth It?

Let’s go back to Sarah and Mark. After losing the first house, they didn’t make the same mistake twice. They secured a Bridge Loan for Real Estate through a local credit union. Three months later, another perfect house popped up. They made a non-contingent offer. They won.

Yes, they paid about $4,000 in interest and fees over the four months it took to sell their old home. But they got the house. They didn’t have to move into a rental. They didn’t have to stress. To them, that $4,000 was a bargain.

Conclusion

Real estate is rarely a straight line. It’s messy. Timelines never line up perfectly. A Bridge Loan for Real Estate is a power tool. It gives you leverage and flexibility in a rigid market. It buys you time, and in real estate, time is often the most valuable asset of all.

If you have strong equity and a solid exit strategy for your current home, don’t let the fear of “two mortgages” scare you away from your dream home. Run the numbers, talk to a lender, and build the bridge.

Are you currently stuck trying to buy and sell at the same time? Drop a comment below—I’d love to hear how you are managing the juggle!

FAQ Section

1. How long does a bridge loan last? Most Bridge Loan for Real Estate terms are short, typically running between 6 months and 12 months. The expectation is that your current home will sell within that window, paying off the loan.

2. Do I have to make monthly payments on a bridge loan? It depends on the lender. Some require monthly interest-only payments. Others allow you to roll the interest into the loan balance, meaning you make zero payments until you sell your old house (balloon payment). This is great for cash flow but eats into your final profit.

3. Can I get a bridge loan with bad credit? It is difficult but possible. Because a Bridge Loan for Real Estate is secured by your property (collateral), some “hard money” lenders care less about your credit score and more about the equity in the home. However, expect to pay much higher interest rates if your credit is below 680.

4. What happens if my home doesn’t sell in time? This is the danger zone. If the term expires, you are in default. You might have to refinance the bridge loan into a standard mortgage (if you qualify) or ask the lender for an extension, which will cost extra fees. Pricing your old home correctly to sell fast is crucial when using a Bridge Loan for Real Estate.

5. Is a bridge loan tax-deductible? Interest on a Bridge Loan for Real Estate can be tax-deductible, similar to mortgage interest, but there are limits based on the total amount of debt and how the funds are used. Always consult a tax professional, as the tax code regarding mortgage interest deduction has changed recently.

6. How fast can I get a bridge loan? Faster than a normal mortgage. Because lenders focus on the asset (the house) rather than a deep-dive into your finances, some hard money bridge loans can close in 2 weeks. Institutional bridge loans might take 30 days. This speed is a huge advantage in competitive markets.